Frankly speaking, there are three stakeholders fighting the guerilla war on online anonymity. These stakeholders are government agencies, cybercriminals, and us, the average internet users. According to a report, 53% of users are skeptical regarding their online protection.

Fortunately, you can use both Blockchain and VPN in parallel to safeguard your digital existence to a new plane. However, you need to know both these innovative technologies and their mutual relationships thoroughly to attain maximum online security.

Without further ado, let us start!

What is Blockchain?

If you do not know what Blockchain is all about, let me clear your misconception. Blockchain technology stores and transfers data or value over the internet. It uses digital signatures along with cryptographic hashing to offer a secure transaction record.

Previously, it was regarded like an accounting tool that transformed into distributed ledger technology (DLT). There is no denying Blockchain has turned out to be a verified procedure for transactions. Let me simplify the whole assertion for you.

I hope you must be aware of Lego blocks. A single block looks like a note that you can assume as an entry that relates to the immediate transaction. However, do you know what happens next when another transaction is made?

When it becomes a part of an entry, it also becomes a part of the database. Moreover, whenever a block is completed, a new block is created. This way, the whole process is repeated for a number of time. Thus, innumerable blocks are tangled with each other in the Blockchain chronologically.

Surprisingly, a block does have a hash of the former block hence the chain attains complete information regarding various user addresses. The information also includes users’ balances from the first block to the recently completed block.

Key Rationale behind Blockchain

The main reason for the creation of the famous distributed ledger technology was to secure users from fraudulent activities. It was developed in order to safeguard your financial transactions that you perform over the internet.

It makes sense as you can make your transactions immutable as these cannot be deleted. The blocks are included with the help of cryptography. As a result, transactions remain middle-proof as you can distribute the data but no one can copy your data.

How Blockchain Works

The Blockchain mechanism works on the assumption of distributed ledger technology hence uses ledger method. Moreover, it empowers cryptocurrencies like Bitcoin by providing next level protection and anonymity. Blockchain stores information through boxes that you can call them blocks.

To clarify Blockchain working in an appropriate way, I give you an example. There are two individuals managing their startup. Yet, the problem arises when they have to decide who is the owner of the property on which the startup is based.

As already mentioned Blockchain applies the ledger approach; you can check the entry mentioned in the ledger. According to this ledger, the first individual was an actual owner of the property. But, after some time the first person sold the property to the second individual due to financial constraints.

The new entry was entered into the ledger and the said process took place on a continual basis. It indicates whenever there is an attempt made to change the ownership of the property, a new entry was added into a ledger.

The whole process occurred frequently until the second person had to sell the property to the first person again. At present, the owner of the property is the first individual as per the record of ledger.

Blockchain and Bitcoin Correlation Explained

Before I explain you Blockchain further, you should know about another interesting notion. Yes, I am talking about latest sensation in town. You have guessed it perfectly. Bitcoin has become one of the most popular cryptocurrencies that allow you to pay your dues anonymously.

Bitcoin is an application based on the Blockchain principle. The principle allows you to implement different applications like solutions and services. Blockchain will help many industries and individuals. Bitcoin that works as a distributed payment system is the prime example.

Furthermore, it is a concrete network made up of miners and nodes too. Let me give you a simple example to simplify the relationship between the two attributes. Bitcoin does work through Blockchain. The latter is the infrastructure, and the former is the asset. Hence, you cannot separate them.

Blockchain is a dispersed public digital ledger that keeps the records of Bitcoin transactions. Similarly, Bitcoin wallet does have the secret piece of data you may call it a private key. The role of private key is a significant one. When it comes to signing transactions through mathematical proof provided by wallet owner, you have to rely on private key.

In more simple words, Blockchain acts like an underlying data structure that helps Bitcoin nodes in verifying the integrity of the Bitcoin ledger. You are bound to maintain and secure the records by cryptocurrency on the Blockchain.

Sectors Affected by Blockchain?

Cryptocurrency has grasped the mainstream attention of privacy seekers from all around the world. Thanks largely to Blockchain technology, you can perform your digital transactions with such ease while sustaining next-level protection.

The impacts of Blockchain phenomenon are not limited to Cryptocurrencies only. The same kind of technology will certainly revolutionize other sectors a great deal shortly. Here is the list of sectors that feel the consequences of Blockchain:

Internet of Things (IoT)

It would not be wrong to say the Internet of Things is the next big thing in this era of digitalization. Still, there are hurdles that may not allow you to improve your digital lifestyle while using different smart gadgets.

During 2015, Samsung and IBM came up with an idea of using Blockchain application ADEPT (Autonomous Decentralized Peer-to-Peer Telemetry). The basic concept of this app revolves around the decentralization of IoT that enables devices to interact with each other hassle-free.

Cloud Storage

Cloud Storage is another sector taking huge benefits from Blockchain approach. Storj is a firm utilizing the said technology to another level. It uses the basic concept to perform open-source cloud storage. Sadly, cloud storage is still anticipating issues like downtime and users’ inaccessibility to their data. Likewise, cloud storage hacking appears to be a major threat that you should not overlook.

Voting

The advantages of Blockchain technology are increasing day by day. The official authorities can opt for the technology to eradicate voting frauds completely. At the same time, they can get the actual information that relates to casted votes.

If you are unable to go to the polling station for any reason, you can cast your votes online. Through Blockchain, you can enjoy the true benefits of online voting solutions instantly.

Banking

Financial institutions like banks are still finding it difficult to overcome identity theft problems. In addition, they are also facing issues like general protection and cost efficiency of transactions too. Once the banking industry starts implementing the Blockchain notion, it can secure its account holders’ data.

Similarly, they will be able to save a handsome amount of money at faster transaction rates.

Implementation of Blockchain Technology by Microsoft

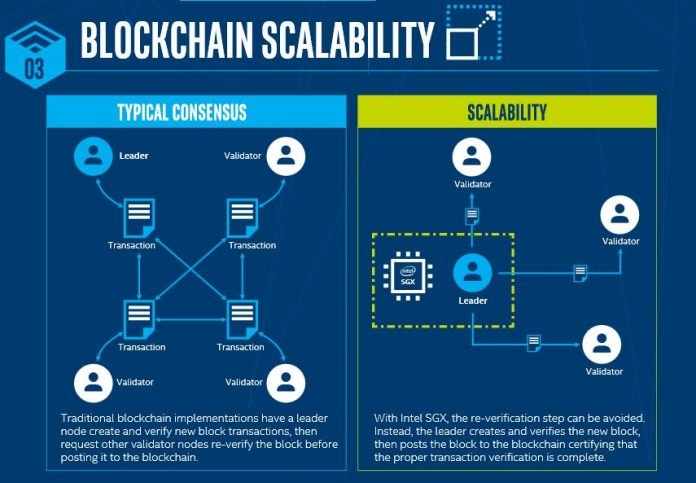

Enterprises are trying to apply the defining concept of Blockchain in a consortium environment. In such environment, there are different groups within the same organization those who want to bypass the drawbacks of a centralized ledger system.

Organizations that have implemented Blockchain technology in true letter and spirit are facing some major issues. Considering the importance of Blockchain, Microsoft has recently introduced an open source framework by the name of Coco.

The said framework will allow businesses to eliminate computer-intensive proofs that induce Bitcoin mining to use huge amount of energy. Consequently, transactions usually take more time than average. Microsoft’s Coco framework provides relief to organizations by swapping the dull work of computation proof.

In order to achieve the objective, the framework offers trusted submissions to the ledger by virtue of creating a trusted execution environment (TEE). If you trust the secure process on your iPhone that stores your fingerprint to perform credit card transactions securely, you must trust the same hardware encryption to safeguard Blockchain transactions.

After inserting Coco code and ledger code both in the secure enclave, no one can see anything that takes place inside the enclave. Likewise, your data and the computation that reside in the enclave are also hidden from the eyes of hackers.

This whole process enables you to construct a trusted network among users in a consortium Blockchain.

What is Bitcoin?

As already mentioned, Bitcoin is a cryptocurrency. You can consider it as a form of electronic cash. You may use them to buy any kind of merchandise anonymously. It does not relate to any country specifically. Bitcoin is not subjected to any regulation too.

What is Bitcoin Wallet?

Bitcoins are typically deposited in a digital wallet. This wallet usually resides in users’ computer systems or in the cloud. You can assume wallet, like a virtual bank account, that you can use to send or receive bitcoins.

What is Ethereum?

Ethereum is an open source software platform that has used the notion of Blockchain technology. It helps developers to create decentralized applications. However, it does not work exactly like Bitcoin. Ethereum is a distributed public Blockchain network like Bitcoin.

What is Ethereum Wallet?

The same applies to Ethereum wallet too. Ethereum is also deposited in a digital wallet. This wallet acts just like software that enables you to store your funds. This way, you can easily perform your desired transactions and check your balance straight away.

Physically, Ethereum wallets do not exist. They are present in the form of records on Blockchain. When you want to conduct a transaction, they interact with Blockchain to complete transactions.

Major Differences between Bitcoin and Ethereum

Still, there are differences that make Ethereum different from Bitcoin. The foremost difference lies in capability and purpose. Bitcoin relies on peer-to-peer electronic cash system that empowers Bitcoin payments. Furthermore, Bitcoin Blockchain helps in tracking the ownership of digital currency.

On the other hand, Ethereum Blockchain enables developers in running programming code of any decentralized application. Interestingly, miners play a crucial role when it comes to earning either a crypto token rather than mining in the case of Bitcoin.

Bitcoin vs Distributed Ledger vs Ethereum vs Blockchain

If you are thinking Blockchain and its related technologies like Bitcoin and Ethereum will take giant leaps in near future, you are correct to certain extent. This is because Blockchain has all the right ingredients to become a leading global public infrastructure.

However, do not confuse yourself when you read the above-mentioned terms with actual product. You may call Blockchain as distributed ledger. It is a next level technology not a product that has been used to develop cryptocurrencies like Bitcoin. The concept of Blockchain is also the backbone of smart contract Ethereum.

Threats and Challenges with Blockchain?

Sadly, some downsides are related with Blockchain that may surprise you a great deal. As per my research, it is a bit tricky to understand the technical terms that have been used in Blockchain technology.

Therefore, a layman will have to come out from his comfort zone to understand the logic behind the famous decentralized mechanism. If you are unable to comprehend encryption and distributed ledgering terms in detail, chances are that you will not attain the desired benefits.

As the technology of blockchain is an idea of a human mind, you should not overlook the pros and cons attached to it. The transfer process of Blockchain financial based models has been beefed-up to new heights. However, the transactions can be easily exposed and stolen at the same time.

Transaction cost is another noticeable factor that you should keep in your mind while using Bitcoin. It only allows seven transactions within a second. You will need to pay $0.20 to perform a single transaction with Bitcoin. Likewise, it only store 80 data bytes per transaction.

Another downside of using Bitcoin is its environmental cost. The energy used by Bitcoin mining is more than the average energy consumed by 159 nations of the world during 2017. Besides, lack of regulation is also causing uncertainty among the minds of users globally.

For instance, Onecoin another cryptocurrency like Bitcoin has robbed millions from investors. In this case, role of legislation does not look quite promising, as it has failed to deliver solutions when such incidents happen.

This situation encourages scammers to take undue advantage. Consequently, they exploit “FOMO” the “fear of missing out” opportunity. When you conduct transactions through Bitcoin or Litecoin, or Ethereum, you cannot eliminate the risk of wallet hacking.

It means you are bound to keep your coins in a wallet, however, at this time these wallets can be exposed to hacking or government crackdowns.

Why VPN is mandatory for Blockchain transactions?

Bitcoin was developed in order to tackle the global financial crisis appropriately. Furthermore, users were able to use an international viable currency digitally that was free from any centralized regulation. Still, you cannot rely on the protection level and anonymity of cryptocurrencies completely.

Blockchain technology offers users with pseudonyms but having said that users’ transactions can be traced. If pseudonyms are coupled with personal information, you may find yourself in hot waters of privacy troubles.

A VPN makes you anonymous while performing Blockchain transactions. It masks your original IP address and spoofs your online locations. Thus, ISPs cannot trace what you do over the internet as you are connected to a VPN provider’s server and use your VPN service’s IP address.

How to Enhance Blockchain Privacy

When you use a VPN service, it enables you to connect your devices be it Windows, Mac, Android and others to a remote server through a tunnel. The tunnel secures and encrypts your data at both ends. Hence, your all information is protected and third parties cannot monitor and keep an eye on your online activities.

It becomes impossible for hackers and ISPs to gather any personal information that is available on Blockchain records. The combination of Blockchain partial anonymity and VPN next level anonymity transforms the overall security of users to unreachable heights.

Luckily, you can also add an additional layer of protection if you follow the below-mentioned tactics:

- You should use a different digital wallet for different kinds of Blockchain payments

- You can encrypt your wallets to make your transactions difficult to trace

- You may keep your payment address confidential that allows you to transfer funds securely

Overcome Region Blocking Hassles

The official authorities in China and South Korea are taking all the necessary steps to curb Bitcoin trading to a certain extent. Both these countries have humongous cryptocurrency markets hence they are implementing cryptocurrency regulations rigorously.

Through geo-restrictions, they are creating hurdles, confining Bitcoin, and other cryptocurrency users a great deal. However, Blockchain users should not lose all their hopes. They can follow the notion of VPN by attaining alternative IP addresses. They can bypass geo-blocking eventually.

Still, there are handfuls of sites availing VPN detection software that track VPN IP addresses and block them. With poly server approach, you can opt infamous VPN services. You can select numerous servers’ IP addresses within the same VPN service.

In this way, you are able to carry out IP address cycling processes on a regular basis. By doing so, you can deceive the VPN detection phenomenon.

Mysterium Blockchain VPN

Mysterium is a decentralized VPN service. The service is an open-source network and based on Blockchain technology. It offers a secure network to users and allows you to rent out your unused network traffic.

Still, it is not a good privacy option to use. Their infrastructure lacks some basic requirements and they have not been able to launch their product in the market. They have just listed their servers on Blockchain. The hackers can gain access to your crucial information by connecting to their preferred servers.

Blockchain and Future of Cyber Security

Blockchain is surely a game changer and has to play a decisive role in coming years. Recently, security vendors from all around the world have started embracing Blockchain solutions according to their own needs.

Organizations like REMME are using Blockchains to a great effect. They can eradicate passwords that are easily hackable due to human error. Through a unique SSL certificate organized by Blockchain to every device, nobody can use fake certificates

Here is how security firms are implementing the notion of Blockchain to deliver solutions to their users:

- Developing peer-to-peer (P2P) consensus procedure to decrease fraud

- Overcoming data tempering issues

- Making sure that there should not be a single point of failure

- Removing human factor from cyber security calculation

Wrapping Up

There is no denying Blockchain is a revolution when it comes to using digital currencies anonymously. It secures your data to some degree but for ultimate privacy, you have to rely on VPN. The combination of Blockchain and VPN is indispensable since the famous technology has downsides that need to be managed.

However, the biggest advantage of using Blockchain technology lies in human error eradication completely from the whole process. But, you need to have the required level of encryption that you will only get through VPN.

If you use a VPN, chances are that you’ll deny online hackers from accessing your crypto wallet or other personal data. Otherwise, you might have to pay the price for your negligence when you perform Blockchain transactions without a VPN.